Top 10 Companies in the Japan HVAC Market

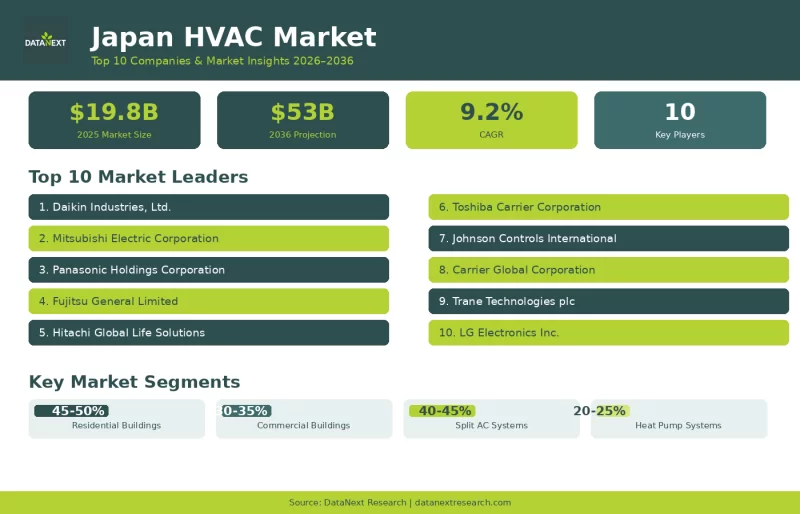

Japan HVAC market is undergoing one of the most significant transformations in its modern history. Valued at USD 19.8 billion in 2025 and projected to reach to USD 53 billion by 2036, the market is growing at a CAGR of 9.2%, driven by a confluence of regulatory ambition, technological innovation, and the urgent demands of a climate-conscious society. Japan's 2050 carbon neutrality target, its ZEH (Net Zero Energy House) mandates, and the Top Runner energy efficiency standards have elevated HVAC systems from mere comfort appliances to critical infrastructure for national decarbonization.

Japan’s aging building stock, where nearly 40% of commercial floor space is over 30 years old, offers a substantial retrofit opportunity for energy-efficient HVAC system upgrades. Concurrently, new construction across Japan’s densely populated urban centers is increasingly characterized by demand for intelligent, integrated climate control systems capable of interfacing with IoT-enabled building management platforms, renewable energy sources, and real-time demand response mechanisms.

Adoption of heat pump technologies is also gaining momentum, supported by government incentive programs that subsidize up to 50% of installation costs in the residential sector. In parallel, the commercial HVAC landscape is being reshaped by expanding infrastructure requirements across data centers, healthcare facilities, and high-rise urban redevelopment projects, particularly within metropolitan hubs such as Tokyo.

Looking for a deeper understanding of how technology shifts, policy frameworks, and retrofit demand are shaping the future of HVAC adoption in Japan?

Explore the full market analysis: https://datanextresearch.com/report/japan-hvac-market

From Japanese industrial champions who invented the modern inverter air conditioner to global building-technology leaders bringing advanced chiller and BMS integration, the competitive landscape of Japan's HVAC market is both deep and dynamic. Here are the top 10 companies shaping its future.

1. Daikin Industries, Ltd.

Daikin Industries, Ltd. is the global market leader in air conditioning systems and maintains a dominant position within Japan’s domestic HVAC industry. Founded in 1924 and headquartered in Osaka, the company has played a foundational role in the development of modern HVAC technologies, including early innovations in split-system air conditioning and inverter-driven compressor systems that have become industry benchmarks for energy efficiency.

Daikin is estimated to hold approximately 30% share of Japan’s residential air-conditioning market, alongside a leading position in the commercial Variable Refrigerant Volume (VRV) segment. Its advanced heat pump platforms, including the Urusara series, are engineered to deliver high Seasonal Coefficient of Performance (SCOP) ratings suited to Japan’s variable climatic conditions, supporting improved residential energy efficiency outcomes.

Within the commercial sector, Daikin’s VRV systems are widely deployed across retrofit and new-build applications, offering measurable reductions in operational energy consumption relative to legacy refrigerant-based installations. The company also offers digital HVAC management platforms such as Mi Cloud, which enable real-time system performance monitoring and predictive maintenance scheduling for commercial building portfolios.

With a workforce exceeding 90,000 employees and operations in more than 150 countries, Daikin reported annual revenues of approximately USD 28 billion. Its integrated building solutions portfolio supports HVAC system optimization through data-driven performance analytics, positioning the company as a provider of end-to-end climate control technologies within Japan’s evolving smart-building ecosystem.

2. Mitsubishi Electric Corporation

Mitsubishi Electric Corporation is one of Japan’s leading HVAC system manufacturers and a globally recognized provider of high-efficiency heating and cooling technologies. The company maintains a strong presence in the domestic commercial segment through its City Multi Variable Refrigerant Flow (VRF) platform, which is widely deployed across high-rise office buildings and mixed-use developments requiring modular scalability and energy-efficient climate control.

The HVAC portfolio of Mitsubishi Electric is complemented by its Lossnay Energy Recovery Ventilation (ERV) systems, which enable heat exchange between incoming and exhaust air streams to improve indoor air quality while reducing energy consumption associated with ventilation loads.

In colder climatic regions such as Hokkaido, the company’s Hyper-Heating INVERTER (H2i) heat pump systems are engineered to maintain heating performance at sub-zero outdoor temperatures, supporting electrified space heating in environments where conventional heat pump technologies may experience efficiency limitations.

The company also offers digital building management solutions such as the MELANS cloud-based control platform, which enables multi-zone HVAC optimization through occupancy-based monitoring and system-level performance analytics across residential and commercial installations.

The HVAC division of the company benefits from the broader expertise in semiconductor technologies and power electronics, enabling tighter integration between inverter hardware and software-based system intelligence. With annual HVAC-related revenues exceeding USD 10 billion, the company continues to invest in R32 refrigerant adoption and the development of low-Global Warming Potential (GWP) solutions aligned with Japan’s regulatory transition toward environmentally sustainable refrigerant technologies.

3. Panasonic Holdings Corporation

Panasonic Holdings Corporation adopts an integrated approach to climate control within Japan’s HVAC market by combining space conditioning, indoor air quality management, humidity control, and residential energy optimization within unified system architectures.

The Aquarea air-to-water heat pump platform of the company has gained traction within Japan’s Net Zero Energy House (ZEH) segment, supporting the electrification of residential heating by replacing conventional gas-based systems with high-efficiency heat pump technologies. Under optimized operating conditions, these systems are capable of delivering Coefficient of Performance (COP) ratings of up to 5.0, contributing to reduced household energy consumption.

The proprietary nanoe™ X air purification technology of Panasonic, which generates hydroxyl (OH) radicals to inhibit airborne pollutants such as viruses, bacteria, and allergens, has seen increased adoption within the residential HVAC segment amid growing awareness of indoor air quality requirements.

The HVAC solutions of the company are also integrated into its broader Home Energy Management System (HEMS) platform, enabling coordinated operation with rooftop photovoltaic (PV) generation and residential battery storage systems. This integration supports improved self-consumption of renewable energy and optimized electricity usage during peak demand periods.

With HVAC solutions contributing to Panasonic’s diversified annual revenues of approximately USD 65 billion, the company continues to invest in product innovation and manufacturing scale to support the deployment of energy-efficient, smart HVAC systems across Japan’s residential and light commercial building segments.

4. Fujitsu General Limited

Fujitsu General Limited maintains a specialized position within Japan’s HVAC market through its focus on application-specific system design tailored to the spatial constraints of high-density urban environments. The company is particularly recognized for compact ceiling-cassette air conditioning units engineered for limited floor-to-ceiling clearances commonly found in commercial office buildings, retail outlets, and hospitality establishments across Japan’s metropolitan centers. Its AIRSTAGE Variable Refrigerant Flow (VRF) platform represents the company’s primary commercial HVAC solution, supporting multi-zone climate control through scalable system configurations, heat recovery functionality, and digitally enabled performance diagnostics accessible via cloud-integrated management interfaces.

Within the residential segment, Fujitsu General’s inverter-based systems, such as the Nocria series, are designed to deliver high seasonal energy efficiency while incorporating integrated humidity sensing and automated filter maintenance features aimed at improving system reliability in high-utilization environments.

The company employs approximately 10,000 personnel globally and generates HVAC-related revenues of nearly USD 3 billion. Its affiliation with Fujitsu Limited provides access to advanced digital capabilities, including AI-enabled system control and edge computing technologies that support adaptive HVAC performance optimization based on real-time building occupancy and usage patterns.

5. Hitachi Global Life Solutions, Inc.

Hitachi Global Life Solutions, Inc., a subsidiary of Hitachi, Ltd., operates at the convergence of HVAC system engineering and smart building intelligence. The company leverages the broader Hitachi Group’s capabilities in IoT infrastructure, artificial intelligence, and integrated digital platforms to deliver climate control solutions aligned with next-generation building performance requirements.

Its Set-Free Sigma Variable Refrigerant Flow (VRF) platform is designed for commercial applications and offers native compatibility with Hitachi’s Lumada digital ecosystem. This integration enables centralized monitoring of energy consumption, predictive fault detection, and automated demand-response functionality across multi-building property portfolios—capabilities that are increasingly relevant within Japan’s smart-city and mixed-use infrastructure developments.

In the residential segment, Hitachi’s Shirokuma-kun inverter air conditioning systems are engineered to deliver stable performance in low-temperature environments while incorporating multi-sensor comfort optimization features for enhanced indoor climate control.

With domestic HVAC-related revenues approaching USD 2.5 billion, Hitachi Global Life Solutions continues to invest in emerging technologies, including hydrogen-compatible heat pump systems and next-generation low-Global Warming Potential (GWP) refrigerants, in alignment with the Hitachi Group’s long-term decarbonization objectives.

6. Toshiba Carrier Corporation

Toshiba Carrier Corporation, a joint venture between Toshiba Corporation and Carrier Global Corporation, combines Japanese engineering capabilities with global HVAC system expertise to serve Japan’s commercial and industrial climate control requirements.

The company maintains a strong presence in Variable Refrigerant Flow (VRF) systems and industrial chiller applications, offering solutions such as the SMMS-e and SMMS-i multi-split platforms for large-scale facilities including hospitals, academic institutions, manufacturing plants, and data centers. These systems are engineered to support heat recovery, zoning flexibility, and operational efficiency across complex building environments.

Toshiba Carrier has also developed specialized expertise in data center cooling technologies, including precision air conditioning and free-cooling solutions designed to improve Power Usage Effectiveness (PUE) metrics in hyperscale and co-location facilities—an increasingly critical requirement amid Japan’s expanding digital infrastructure landscape.

Supported by manufacturing operations in Shizuoka and a nationwide service network, the company provides localized technical support alongside advanced system integration capabilities derived from its parent organizations. With annual revenues in Japan’s commercial HVAC segment exceeding USD 1.5 billion, Toshiba Carrier continues to invest in next-generation chiller efficiency and low-Global Warming Potential (GWP) refrigerant technologies aligned with evolving sustainability standards.

7. Johnson Controls International plc

Johnson Controls International plc delivers integrated building technology solutions within Japan’s HVAC market, with a primary focus on large-scale commercial, institutional, and industrial facilities. The company’s YORK® chiller platforms, York Affinity™ VRF systems, and Metasys® Building Management System (BMS) are deployed across premium infrastructure environments, including healthcare campuses, hospitality properties, and government facilities.

The competitive differentiation of Johnson Controls in the Japanese market is anchored in its OpenBlue digital platform—an AI-enabled ecosystem that integrates HVAC, fire safety, security, and energy management systems across multi-site property portfolios. This unified interface enables real-time performance monitoring, predictive maintenance, and automated energy optimization to support improved operational efficiency.

Such digital integration capabilities assist building operators in managing Scope 2 emissions in alignment with national regulatory frameworks, including provisions under Japan’s Building Energy Conservation Act.

With global revenues exceeding USD 23 billion and an established local presence across Japan’s engineering and service ecosystem, Johnson Controls combines in-country project delivery capabilities with access to global R&D resources. This positioning supports the deployment of low-Global Warming Potential (GWP) refrigerant technologies and district energy integration solutions across complex commercial infrastructure developments.

8. Carrier Global Corporation

Carrier Global Corporation, established as an independent entity following its separation from United Technologies in 2020, participates in Japan’s HVAC market through a diversified portfolio spanning residential, light-commercial, and large-scale applied commercial systems. The company’s product offerings are delivered through both the Carrier and Toshiba Carrier brands, enabling coverage across multiple end-user segments.

The AquaForce® and AquaEdge® centrifugal chiller platforms of Carrier are deployed in high-capacity commercial cooling applications, including office complexes, healthcare facilities, and data centers, where system efficiency and operational reliability are critical.

The company has also advanced the deployment of equipment utilizing low-Global Warming Potential (GWP) refrigerants, such as R-1234ze, in alignment with Japan’s regulatory phase-down of high-GWP fluorocarbons under the revised Fluorocarbons Recovery and Destruction Law.

Through its Carrier-i digital diagnostics platform, Carrier provides remote performance monitoring and predictive maintenance capabilities aimed at improving equipment uptime and extending asset lifecycle performance.

With global annual revenues of approximately USD 21 billion and ongoing technical collaboration through its joint venture with Toshiba Carrier Corporation, Carrier combines international product development resources with localized operational support. The company’s commitment to achieving net-zero emissions from its own operations by 2050 further aligns its HVAC solutions portfolio with sustainability objectives within Japan’s built environment.

9. Trane Technologies plc

Trane Technologies plc adopts a sustainability-oriented approach within Japan’s commercial and industrial HVAC market, positioning its Trane® and Thermo King® brands as premium solutions for clients seeking improved lifecycle cost efficiency and reduced carbon intensity across building operations.

The CenTraVac® centrifugal chiller systems of the company are widely recognized for high operational efficiency in large-scale cooling applications, while the Tracer SC+ building automation platform enables detailed energy monitoring, system-level diagnostics, and automated optimization across multi-building commercial portfolios.

Trane Technologies has also established emissions-reduction commitments through its Gigaton Challenge, which targets the avoidance of one billion metric tons of carbon emissions from customer operations by 2030. This initiative aligns with Japan’s increasing emphasis on corporate sustainability reporting and environmental, social, and governance (ESG) disclosure frameworks.

With global revenues of approximately USD 18 billion, Trane Technologies continues to expand its presence in Japan through investments in natural refrigerant-based heat pump systems, humidity management technologies suited to the country’s seasonal climate conditions, and district energy consulting services designed to enhance energy efficiency across urban infrastructure developments.

10. LG Electronics Inc.

LG Electronics Inc. has established an expanding presence in Japan’s HVAC market through sustained investment in system efficiency, digital connectivity, and application-specific product development. While initial market entry was driven by competitively priced residential solutions, the company has progressively broadened its portfolio to include advanced commercial platforms such as the Multi V 5 Variable Refrigerant Flow (VRF) system.

LG’s HVAC offerings benefit from the company’s capabilities in semiconductor technologies and AI-enabled control systems, enabling inverter-driven compressor optimization and integration with its ThinQ™ smart connectivity platform. These features support interoperability with broader smart-home ecosystems across residential applications.

The Therma V™ air-to-water heat pump series of the company, engineered for high-efficiency heating performance under low ambient temperatures, has gained traction within Japan’s Net Zero Energy House (ZEH) segment as an electrified alternative to gas-based heating systems.

With global HVAC-related revenues exceeding USD 7 billion and R&D investment of approximately 6% of annual sales, LG continues to strengthen its localized manufacturing, distribution, and service capabilities aligned with Japanese market requirements. The company’s adoption of R32 and R290 refrigerants across expanding product lines further supports compliance with Japan’s evolving regulatory framework for environmentally sustainable refrigerant technologies.

The insights presented above are derived from our in-depth strategic assessment of Japan’s HVAC ecosystem, covering:

- Market sizing and 10-year forecasts

- Heat pump and VRF technology outlook

- ZEH/ZEB retrofit demand trends

- Competitive benchmarking of key manufacturers

- Regulatory and refrigerant transition analysis

Download a free sample of the full report to evaluate its scope:

https://datanextresearch.com/report/japan-hvac-market?action=Download+Sample

Engineering Japan's Climate-Resilient Future

Japan HVAC market is being shaped by a unique combination of factors: stricter energy efficiency regulations, an aging building stock that requires large-scale upgrades, diverse climatic conditions across different regions, and end-users who place a strong emphasis on reliability and performance over the long term.

The ten companies highlighted in this report reflect the diversity of the competitive landscape, from Daikin’s leadership in residential air-conditioning systems to Johnson Controls’ integrated solutions for large commercial buildings, from Mitsubishi Electric’s cold-climate heat pump technologies to LG Electronics’ smart-home compatible HVAC platforms. Each of these companies addresses specific needs across Japan’s residential, commercial, and industrial infrastructure segments.

The growth of this market from USD 21.4 billion in 2026 to USD 53 billion by 2036 will be driven by several long-term trends, including increasing adoption of heat pump-based heating systems, the expansion of smart and connected HVAC technologies, the shift toward low-Global Warming Potential (GWP) refrigerants, and the modernization of older residential and commercial buildings.

As Japan progresses toward its 2050 carbon neutrality goals, the HVAC sector is expected to play a central role in improving energy efficiency across the built environment. The deployment of high-efficiency heat pumps, digitally managed climate control systems, and environmentally sustainable refrigerants will collectively contribute to reducing energy consumption and emissions from buildings.

In this context, HVAC systems are becoming more than comfort-enabling technologies. They are evolving into essential infrastructure components that support Japan’s transition toward energy-efficient, climate-resilient urban development.

For stakeholders evaluating opportunities in Japan’s rapidly evolving building infrastructure market, our comprehensive Japan HVAC Market (2026–2036) report provides detailed insights into:

- Growth outlook from USD 21.4 billion in 2026 to USD 53 billion by 2036

- Heat pump electrification trends

- Smart HVAC and IoT integration

- Low-GWP refrigerant transition

- Commercial retrofit opportunities

Access the full report here: Japan HVAC Market – Request Full Report

Or download a sample to review the methodology and coverage: https://datanextresearch.com/report/japan-hvac-market?action=Download+Sample

Related Articles

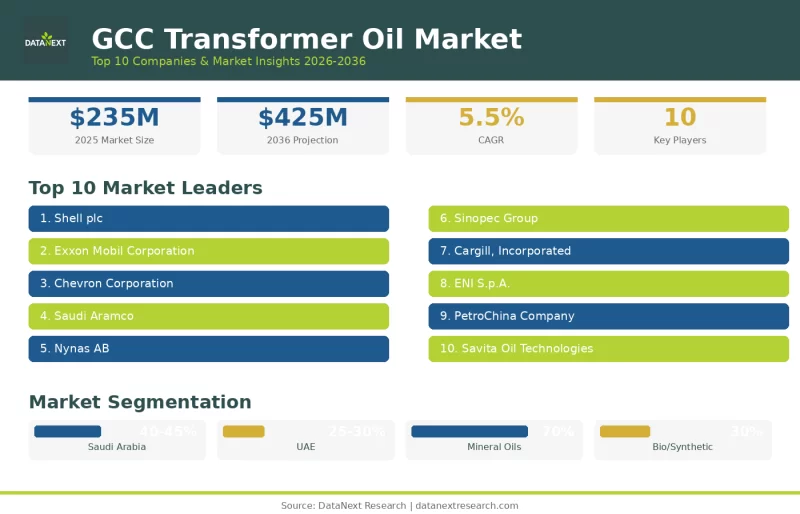

Top 10 Companies in the GCC Transformer Oil Market

Discover the top 10 companies in the GCC transformer oil market driving growth to 2036. Explore leaders like Shell, ExxonMobil, Chevron, and more shaping grid modernization, insulating fluid tech, and renewable energy integration.