Best Food Processing Companies in Europe (Top 10) | Market Leaders & Innovation

Overview of Europe’s Food Processing Industry

The European food processing sector is today positioned between established food habits and world class innovation. It delivers food to millions every day, provides global brands, and increasingly meets consumer needs for healthy, transparent, and sustainable food. The food processing sector includes dairy and meat processing, confectionery and snacks, beverages, ingredients, as well as specialized nutrition.

European food processors enjoy the benefits of close ties with high-quality agricultural input suppliers, modern manufacturing technology, and highly regulated markets with strict safety and quality regulations, factors that enhance both domestic and international market acceptance.

Top 10 Food Processing Companies in Europe:

1. Nestlé S.A. – Market Leadership & Nutrition Strategy

Nestlé remains the world’s largest food and beverage company, with a vast portfolio spanning coffee (Nescafé, Nespresso), confectionery (KitKat, Smarties), infant nutrition (Gerber), prepared foods (Maggi, Stouffer’s), dairy, and pet care (Purina). In 2024, the company delivered CHF 91.4 billion in sales, achieving organic growth of 2.2% despite a challenging consumer environment. Growth was fueled by coffee, confectionery, and pet care, with Europe and emerging markets outperforming some mature regions.

Nestlé continues to sharpen its focus on nutrition, health, and wellness, restructuring to prioritize higher-growth categories and innovation. Sustainability remains central: by the end of 2023, nearly 92% of global manufacturing electricity came from renewable sources, and Nestlé is accelerating regenerative agriculture initiatives across its supply chain.

Financially, Nestlé demonstrates resilience with strong free cash flow (CHF 10.7 billion) and a long history of dividend growth, reinforcing its ability to invest in strategic priorities while rewarding shareholders.

Looking ahead, Nestlé expects organic growth in the mid-single-digit range and a moderate improvement in operating margin, supported by:

- Continued momentum in coffee, pet care, and premium nutrition.

- Expansion in emerging markets, which remain a key growth engine.

- Ongoing portfolio optimization and cost-efficiency programs.

- Accelerated progress on sustainability goals, including regenerative agriculture and emissions reduction.

Nestlé’s strategy for 2025 centers on innovation, premiumization, and digital engagement, aiming to strengthen its leadership in health-focused and sustainable food solutions.

2. Unilever PLC – Power Brands and Portfolio Focus

Unilever remains one of the most diversified consumer goods companies globally, combining food and refreshment brands with personal care and home care. In 2024, the company delivered €60.8 billion in turnover, supported by underlying sales growth of 4.2%, driven largely by volume gains. Its Food & Refreshment segment includes household names such as Hellmann’s, Flora, and Blue Band, alongside tea brands like Lipton (through joint ventures) and premium ice cream labels such as Magnum and Ben & Jerry’s. To sharpen its strategic focus, Unilever announced plans to separate its ice cream business into a standalone entity. The company’s growth strategy centers on simplifying its portfolio, scaling core “Power Brands,” and embedding sustainability across operations from reducing packaging waste and increasing recycled content to advancing plant-based innovations.

Looking ahead, Unilever expects mid-single-digit underlying sales growth and continued margin improvement, supported by disciplined cost management and reinvestment in innovation. Strategic priorities include accelerating the spin-off of the ice cream division, driving premiumization in food and refreshment, and deepening its sustainability commitments such as achieving higher recycled content in packaging and expanding plant-based offerings. These initiatives aim to strengthen Unilever’s competitive edge while delivering consistent shareholder returns in a challenging global market.

3. Danone S.A. – Health, Dairy & Plant-Based Leadership

Danone has long been known for its focus on health-driven dairy, plant-based products, specialized nutrition, and bottled water. In 2024, under its “Renew” strategy, the company delivered €27.4 billion in sales, with like‑for‑like growth of 4.3% driven by a 3% rise in volumes and a 1.3% lift in prices. Profitability also strengthened with the recurring operating margin increased to 13.0%, recurring earnings per share rose by 2.5%, free cash flow reached €3 billion (a 14% increase), and net debt fell, underlining strong cash conversion.

Danone’s standout brands include probiotic yogurts like Activia, plant-based alternatives such as Alpro, and high-end infant and medical nutrition lines. It has also earned global B Corp certification across over 200 legal entities in more than 60 countries, highlighting its commitment to social and environmental best practices.

Innovation is fueled by probiotic science and plant-based development, while sustainability initiatives span regenerative agriculture and sustainable packaging in tune with health- and eco-conscious consumer trends.

Danone reaffirmed its guidance for 3–5% like-for-like sales growth, with recurring operating income expected to grow faster than sales, reflecting confidence in its health-focused portfolio, disciplined cost management, and acquisition-driven growth.

4. Mondelēz International – Europe’s Snacking Powerhouse

Mondelēz International, though headquartered in the U.S., has deep roots in Europe and remains a dominant force in the confectionery and snack market in the region. Beloved brands such as Milka, Côte d’Or, Toblerone, Cadbury, and Oreo underscore its strong local relevance. Guided by its “Snacking Made Right” philosophy, Mondelēz focuses on portion control, transparent ingredients, and sustainable sourcing, particularly through its Cocoa Life program, which promotes ethical cocoa farming. European manufacturing hubs in Switzerland and Belgium combine artisanal heritage with global scale, reinforcing quality and efficiency. While commodity cost pressures, especially cocoa, pose challenges, Mondelēz continues to leverage its powerful brand equity and innovation to maintain leadership in the snacking category.

5. Ferrero Group – Premium Confectionery Excellence

Ferrero is a family-owned confectionery powerhouse with a global footprint rooted in European craftsmanship. Its iconic brands such as Nutella, Ferrero Rocher, Kinder, and Tic Tac are cultural staples that have built deep emotional connections with consumers worldwide. Growth at Ferrero combines product excellence with strategic acquisitions, such as Thorntons and parts of Nestlé’s confectionery business, expanding both market share and category reach. The company emphasizes premium positioning and brand storytelling to maintain its leadership in indulgent treats.

The sustainability agenda is equally strong, targeting 100% segregated sustainable palm oil and advancing broad cocoa sustainability programs to ensure ethical sourcing and meet rising consumer expectations for responsible products. Looking ahead, Ferrero is expected to continue leveraging its heritage of quality and innovation while investing in sustainability and premiumization, key pillars that will help it navigate cost pressures and reinforce its status as one of the world’s most trusted confectionery brands.

6. Associated British Foods – Ingredients & Grocery Strength

Associated British Foods (ABF) is a diversified leader in food processing and ingredients, with a strong presence across multiple categories. While widely recognized for its Primark retail arm, ABF’s food business is substantial and strategically important. In 2024, the company reported £20.07 billion in revenue, supported by its broad portfolio that spans sugar processing (British Sugar, Illovo), grocery staples like Twinings tea, Ovaltine, Jordans cereals, and Ryvita, as well as a robust ingredients division supplying emulsifiers, enzymes, and yeasts. This vertical integration—from agriculture to specialty ingredients—provides resilience against commodity volatility, while heritage brands balance tradition with innovation.

Looking ahead to 2025, ABF aims to deliver steady growth through operational efficiency, disciplined cost management, and continued investment in its grocery and ingredients businesses. Strategic priorities include expanding sustainable sourcing practices, driving innovation in health-focused products, and leveraging its integrated supply chain to maintain competitiveness. These initiatives position ABF to navigate market challenges while reinforcing its reputation as a stable, diversified food industry player.

7. Arla Foods – Cooperative Dairy Model in Europe

Arla Foods is a farmer-owned cooperative and a leading name in European dairy, known for fresh milk, butter under the Lurpak brand, specialty cheeses like Castello, and a wide range of yogurts. In 2024, Arla reported revenues of around €13.8 billion, reflecting the resilience of dairy demand and stable pricing trends. Its cooperative structure ensures strong farmer engagement and underpins sustainability initiatives, including methane reduction and improved farming practices. Arla continues to innovate with organic, high-protein, and lactose-free products, while investing in sustainable packaging to meet evolving consumer expectations.

Looking ahead to 2025, Arla aims to strengthen its position through premiumization, health-focused innovation, and climate-friendly farming. Strategic priorities include accelerating progress on carbon reduction, expanding its portfolio of functional and plant-based dairy alternatives, and leveraging digital tools for supply chain efficiency. These efforts position Arla to balance cooperative values with competitive growth in a dynamic European dairy market.

8. FrieslandCampina – Dairy Ingredients & Consumer Brands

FrieslandCampina is one of Europe’s largest dairy cooperatives, combining farmer ownership with global reach. In 2024, the company generated approximately €12.9 billion in revenue, driven by a mix of consumer brands and high-value dairy ingredients. Regional favorites such as Campina, Friesche Vlag, and Dutch Lady maintain strong resonance in home markets, while its ingredients division supplies proteins and functional dairy components to food manufacturers worldwide. This dual focus on branded products and B2B solutions provides resilience and growth opportunities.

Sustainability is deeply embedded in FrieslandCampina’s strategy, with initiatives targeting farm-level climate impact reduction, improved biodiversity, and regenerative practices—all aligned with evolving consumer and regulatory expectations. Looking ahead to 2025, the cooperative plans to accelerate innovation in high-protein, functional nutrition, and plant-based dairy alternatives, while continuing to invest in carbon reduction and circular packaging solutions. These priorities position FrieslandCampina to balance cooperative values with competitive performance in a rapidly changing global dairy landscape.

9. Barry Callebaut – Global Chocolate & Cocoa Leader

Barry Callebaut is the world’s leading supplier of chocolate and cocoa ingredients, serving as a critical partner to major confectionery and snack brands across Europe and globally. Its products form the foundation of countless chocolates and sweet treats, reinforcing its position as an indispensable player in the industry. The company’s Forever Chocolate program underscores its commitment to sustainability, focusing on responsibly sourced cocoa, improving farmer livelihoods, and eliminating child labor—key priorities given the complexity of cocoa supply chains. Innovation remains central, with Barry Callebaut introducing sugar-reduced and plant-based chocolate formulations alongside new flavor variants to meet growing consumer demand for healthier indulgence.

Looking ahead to 2025, Barry Callebaut aims to strengthen its leadership through continued investment in sustainable sourcing, advanced processing technologies, and premium product development. Strategic priorities include expanding its plant-based portfolio, accelerating climate-positive initiatives, and deepening partnerships with global brands to deliver ethical, high-quality chocolate solutions. These efforts position Barry Callebaut as a forward-thinking leader in a market balancing indulgence with responsibility.

10. Kerry Group – Taste & Nutrition Solutions Specialist

Kerry Group, headquartered in Tralee, Ireland, is a global leader in taste and nutrition solutions, partnering with food and beverage manufacturers to deliver flavor systems, functional ingredients, and technical expertise. In 2023, the company reported revenues of about €8.0 billion, underpinned by its broad portfolio spanning dairy solutions, flavor technologies, and nutrition systems that help brands innovate. Kerry’s taste solutions enable manufacturers to reduce salt and sugar without compromising flavor, while its functional ingredients support plant-based, fortified, and clean-label products—key trends shaping modern consumer preferences.

Sustainability is embedded across Kerry’s operations, with initiatives targeting water and energy efficiency, responsible sourcing, and supply chain transparency. Looking ahead to 2025, Kerry aims to accelerate growth through advanced flavor innovation, expansion in emerging markets, and deeper integration of health-forward solutions. Strategic priorities include scaling plant-based and protein-rich offerings, investing in digital tools for formulation, and driving progress toward its environmental goals. These efforts position Kerry as a critical enabler of food industry transformation, balancing taste, nutrition, and sustainability.

Key Innovation Trends in the European Food Processing Market:

Across these leading players, certain innovation themes stand out:

- Plant-Based and Alternative Proteins

European consumers are rapidly embracing plant-based foods for health and environmental reasons. Leading processors are investing in improved taste, texture, and nutrition for dairy and meat alternatives, often partnering with startups or research institutions to refine ingredient technologies.

- Personalized and Functional Nutrition

From gut health probiotics to fortified foods and tailored nutrition products, European companies are responding to consumer interest in foods that do more than satiate hunger — they support wellness goals.

- Sustainability & Regenerative Practices

Sustainability is now mainstream: companies pursue regenerative agriculture, carbon reduction, circular packaging, and food-waste minimization. Forward-thinking processors embed these principles deep into strategy rather than treating them as add-ons.

- Digital & Industry 4.0

Advanced data analytics, AI, IoT sensors, and machine learning are improving quality control, supply chain transparency, and product innovation. Blockchain traceability helps consumers verify claims about origin, safety, and sustainability.

- Clean Label & Transparency

Consumers increasingly demand simpler ingredient lists and clear information. Leading processors respond by reformulating products, improving packaging communication, and securing third-party certifications (e.g., organic, fair trade).

Strategic Challenges Facing European Food Manufacturers:

- Raw Material Volatility

Commodity price swings—from cocoa to dairy feed—continue to pressure margins. Companies must strengthen risk management, diversify sourcing, and deepen partnerships with farmers to ensure supply stability.

- Nutrition & Health Regulations

Evolving rules on front-of-pack labeling, sugar taxes, and marketing restrictions are reshaping product portfolios. Reformulation toward healthier profiles and transparent communication is no longer optional—it’s a competitive necessity.

- Retail Evolution

The rise of e-commerce, private-label growth, and retail consolidation demands agile, omnichannel strategies. Brands need differentiated value propositions and digital engagement to stay relevant in a fragmented retail landscape.

- Competition & Consolidation

Intensifying competition from startups, private labels, and global players is driving consolidation. Strategic acquisitions and partnerships can accelerate growth, but successful integration and cultural alignment remain critical to unlocking value.

Future Outlook of the European Food Processing Industry:

Europe’s food processing industry is a dynamic blend of heritage and innovation. From global giants like Nestlé to farmer-owned cooperatives such as Arla and FrieslandCampina, leading players are investing heavily in quality, sustainability, and consumer-centric strategies. The future will be shaped by digital transformation, climate-conscious practices, and product innovation that supports both health and environmental goals. Companies that successfully balance tradition with forward-thinking solutions, embracing technology, ethical sourcing, and nutrition-led portfolios, will define the next chapter of growth in this evolving landscape.

Looking for deeper insights into the European food processing market?

Explore our industry reports covering market size, competitive landscape, investment trends, and growth opportunities across Europe.

Related Articles

Top 10 Companies in the Latin America Organic Coffee Market

Discover the top 10 organizations driving Latin America’s organic coffee market (2026–2036). Explore leaders like FNC, Olam, ECOM, and Cooxupé shaping sustainable, traceable, and premium Arabica supply.

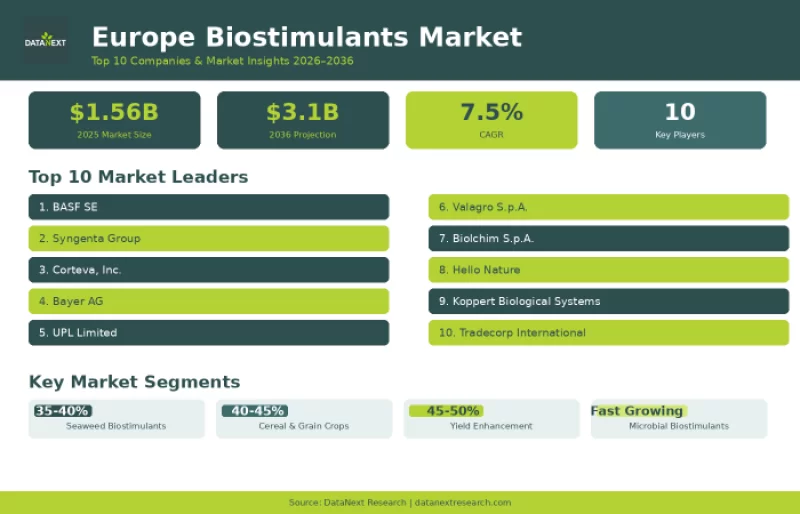

Top 10 Companies in the Europe Biostimulants Market

Discover the Top 10 Companies in the Europe Biostimulants Market driving growth to USD 3.1B by 2036. Explore leaders like BASF, Syngenta, Corteva, and more shaping sustainable crop inputs, plant growth, and stress resilience across European agriculture.